Yes, you absolutely do pay tax on rental income in the UK. Think of it just like any other source of earnings, such as a salary from your job – it all needs to be declared to HMRC. The crucial thing to remember is that you're taxed on your rental profit, not the total amount of rent you collect.

Your Quick Guide to UK Rental Income Tax

Stepping into the world of being a landlord is a big move. While it can be a great investment, it also comes with new responsibilities, and getting your head around tax is right at the top of the list.

The system might look a bit daunting at first, but the core idea is straightforward. You pay Income Tax on the profit left over after you’ve subtracted your legitimate, day-to-day running costs from the rental income you’ve received.

This rental profit is then added to any other income you have (like your main job’s salary) to work out which tax band you’re in. The whole process is managed through the Self Assessment system, and if you’re earning money from property, filing a return is a must.

Who Needs to Pay Tax?

It's simple: if you receive income from renting out a property you own, you are legally required to declare it. This rule applies whether you're letting out a single room in your home or managing an entire portfolio of properties. The scale of your rental business doesn’t change that fundamental obligation.

For the 2023 to 2024 tax year, official figures show that 2.86 million unincorporated landlords declared rental income via Self Assessment. Your profits are taxed at the same Income Tax rates as other earnings: 20% (basic rate), 40% (higher rate), or 45% (additional rate), depending on your total income for the year.

However, if you're just dipping your toe in the water, you might be able to use the £1,000 Property Allowance, which makes small amounts of rental income tax-free. You can dig into the specifics by checking the latest government statistics on property rental income.

Getting your tax obligations right from day one is non-negotiable. If you fail to declare your rental income, HMRC can hit you with some hefty penalties and interest charges, quickly turning what should have been a profitable venture into a very expensive lesson.

To give you a clear, immediate overview, here’s a quick summary of the essential facts every landlord needs to know.

UK Rental Income Tax at a Glance

This table breaks down the core elements of the UK's rental income tax system, providing a handy reference point for landlords, whether you're just starting out or have been doing this for years.

| Element | Key Information |

|---|---|

| Who Pays Tax? | Anyone in the UK receiving income from renting out property. |

| What is Taxed? | The profit you make (Total Rent minus Allowable Expenses). |

| Tax Rates (2024/25) | 20%, 40%, or 45%, depending on your total income band. |

| Key Allowances | The £1,000 tax-free Property Allowance for small incomes. |

| How to Report | Via a Self Assessment tax return submitted to HMRC. |

| Online Filing Deadline | Midnight on 31st January following the end of the tax year. |

As you can see, the principles are quite clear. The next step is understanding exactly what counts as income and, just as importantly, what you can claim as an expense to reduce that final tax bill.

What HMRC Actually Considers Rental Income

When you think about rental income, your mind probably jumps straight to the monthly rent hitting your bank account. And while that's the main event, it's not the whole story from HMRC's perspective. Their definition is a lot wider, and getting to grips with it is key to reporting your earnings correctly and avoiding any unwelcome surprises later on.

The best way to look at it is to treat your rental property like any other business. The income isn't just the rent; it's all the money the property generates. This means any payment you get from a tenant as part of their tenancy could be classed as taxable income.

It's a common mistake for new landlords to miss some of these extra income streams. HMRC needs a full picture of everything you've earned from the property before you can start deducting your expenses to work out your profit. Let's break down exactly what that includes.

Income You Must Declare

Your total rental income is the grand total of everything your tenants have paid you for living in the property and using any services you provide. Some of these are obvious, but others are easy to forget.

Here’s what HMRC will be looking for on your tax return:

- Rent Payments: This is the big one – all the regular rent you've received from your tenants throughout the tax year.

- Non-refundable Deposits: If you take a holding deposit to reserve a property and the tenant doesn't get it back, that counts as income. This is different from the main security deposit, which we'll get to in a moment.

- Income from Services: Do you charge extra for things like cleaning, gardening, or even utilities? If so, that money is part of your rental income.

- Balancing Charges: This is a bit more technical, but it can pop up if you sell or dispose of an asset (like a piece of equipment) that you’ve previously claimed capital allowances on.

- Income from Furniture: If you let a furnished property and charge a separate fee for the use of the furniture, that counts as rental income too.

Keeping detailed records of every single payment you receive is absolutely essential. It makes filling out your Self Assessment so much easier and ensures nothing gets missed.

What Is Not Considered Rental Income

Knowing what doesn't count as income is just as important, as getting this wrong could mean you end up overpaying tax. The main one to remember here is the tenant's security deposit.

A refundable security deposit (often called a tenancy deposit) is not your income. That money technically still belongs to the tenant and must be protected in a government-approved scheme. It only becomes your income if you have a legal right to keep some or all of it—for instance, to pay for repairs after the tenancy ends.

By understanding both sides of the coin—what is income and what isn't—you can build a true financial picture of your property business. This is the foundation you need before moving on to the next step: subtracting your allowable expenses to find your actual taxable profit.

How Allowable Expenses Can Reduce Your Tax Bill

Once you’ve figured out your total rental income for the year, we get to the part where you can legally and proactively shrink your tax bill. This is all about deducting your allowable expenses—the day-to-day costs you have to pay to keep your rental property running smoothly.

It helps to think of your property as a small business. The rent you collect is your turnover, but all the money you spend on repairs, agent fees, and insurance are your business running costs. HMRC lets you subtract these essential costs from your income, so you’re only taxed on your actual profit.

Knowing exactly what you can and can’t claim is crucial. Meticulous records can be the difference between paying the right amount of tax and giving HMRC far too much of your hard-earned money. To get the most out of this, it's worth understanding the full scope of what you can claim; a comprehensive guide to rental property tax deductions can offer a wider view on the subject.

Property Maintenance and Repairs

This is a big one. It covers everything you spend to keep the property in a safe and liveable state for your tenants. The key here is to understand the difference between a 'repair' and an 'improvement', because HMRC treats them very differently.

- Repairs: These are fully tax-deductible. A repair simply brings something back to its original working condition. Think like-for-like replacements: fixing a leaky tap, mending a fence panel that blew down in a storm, or repainting a wall to cover wear and tear.

- Improvements: These are not tax-deductible against rental income. An improvement makes the property better than it was before. Examples include building an extension, upgrading a basic kitchen to a high-spec one, or adding a conservatory. These are classed as 'capital expenditure' and come into play later to reduce your Capital Gains Tax bill when you sell.

Analogy: Imagine your rental has a few cracked roof tiles after a bad winter. Replacing just those tiles is a repair, and you can claim the cost. But if you decide to rip off the whole roof and replace it with premium Spanish slate, that’s an improvement. You can't deduct that from your rental income.

Professional Fees and Running Costs

It's not just about bricks and mortar. The admin and professional services you pay for are also fully deductible expenses that keep your rental business afloat.

Here are some of the most common running costs you can claim:

- Letting agent and management fees: The commission you pay an agent to find a tenant or manage the property for you.

- Accountant's fees: The cost of hiring an expert to handle your tax return and make sure you're compliant.

- Legal fees: Essential costs for things like drafting tenancy agreements or, if necessary, handling an eviction.

- Landlord insurance: The premiums you pay for buildings, contents, and public liability cover.

- Direct running costs: Any utility bills (gas, electricity, water) or council tax you have to cover yourself during void periods when the property is empty.

For a deeper dive into everything you can claim, check out our complete guide to rental property allowable expenses.

The £1,000 Property Allowance Alternative

If you're a landlord with just one property and very few expenses, HMRC offers a much simpler route: the £1,000 property allowance.

This is a flat, tax-free allowance. If your total rental income for the tax year is under £1,000, you don't even need to declare it. Simple.

If your income is over £1,000, you have a choice. You can either add up and deduct all your actual expenses, or you can just deduct the flat £1,000 allowance instead. You just pick whichever option saves you more money. It’s perfect for landlords whose actual costs are low, as it saves you the admin of tracking every single receipt.

A Special Note on Mortgage Interest

This is one of the biggest changes for landlords in recent years and catches a lot of people out. You can no longer deduct your mortgage interest payments from your rental income like a normal expense.

Instead, you now get a tax credit worth 20% of your annual mortgage interest. This credit is used to reduce your final tax bill directly, rather than reducing your taxable profit.

The crucial point is that this change hits higher and additional-rate taxpayers the hardest. They used to get tax relief at 40% or 45%, but now everyone, regardless of their income, gets the same basic-rate 20% credit. This often means landlords in higher tax bands are now paying significantly more tax than they did under the old system.

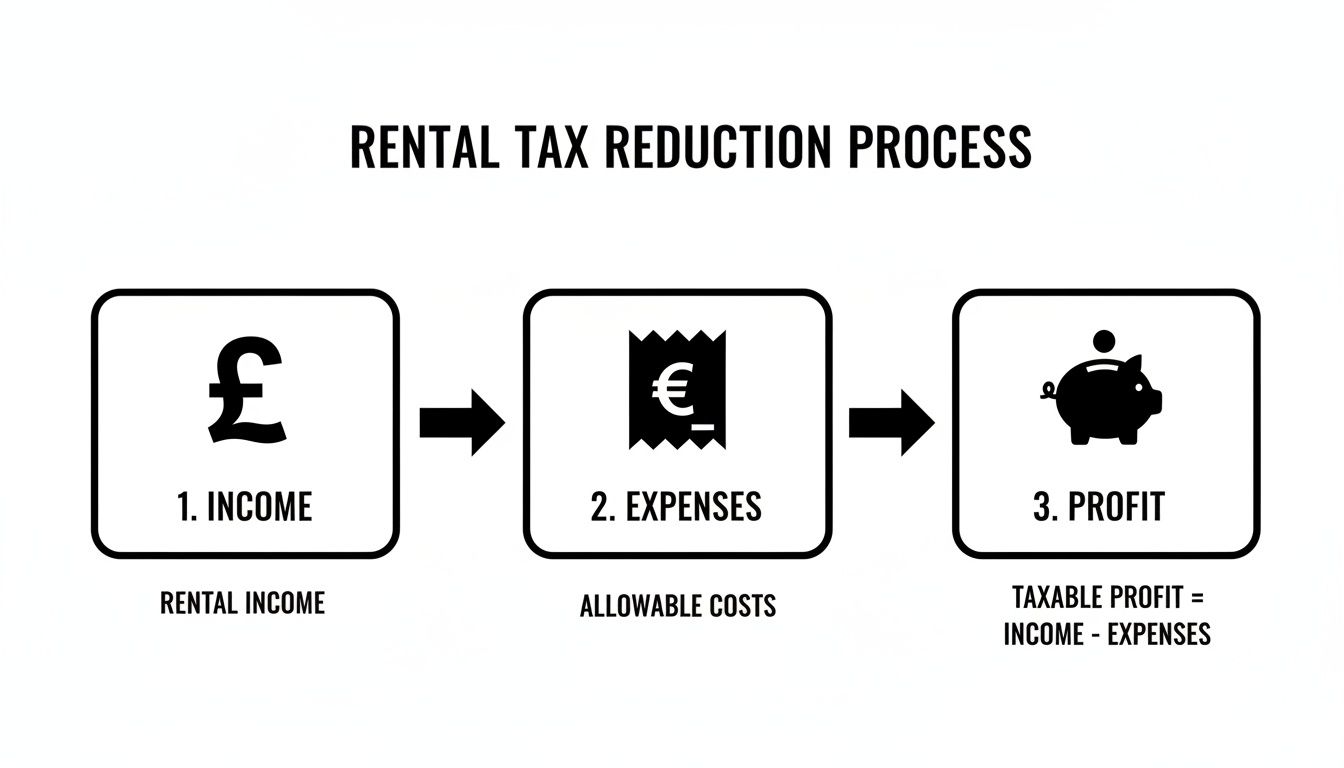

Calculating Your Rental Income Tax Step by Step

Theory is one thing, but seeing the numbers in action is where it all clicks. Let's walk through exactly how you calculate the tax on your rental income, starting with the simple formula at the heart of it all.

At its core, the calculation is straightforward: Total Rental Income – Allowable Expenses = Taxable Profit. This is the figure that gets added to your other income (like your salary) to work out what you owe HMRC.

This flowchart breaks down the simple three-step journey to finding your taxable profit.

As you can see, you start with your total rent collected, subtract your legitimate costs, and are left with the profit that's subject to tax. Keeping track of all this can be tricky, especially if you have rent coming into different accounts. Using a good bank statement converter software can make gathering and organising this information much simpler.

Let's look at a few real-world scenarios to see how this plays out.

Example 1: The Basic Rate Taxpayer

Meet Sarah. She has a full-time job and rents out a small flat on the side.

- Annual Rental Income: £12,000

- Allowable Expenses (repairs, agent fees, insurance): £2,500

- Annual Mortgage Interest: £4,000

First, we need to find her rental profit:

£12,000 (Income) – £2,500 (Expenses) = £9,500 (Taxable Profit)

This £9,500 profit gets added to her salary. Since she's a basic rate taxpayer, she pays 20% tax on this amount, which comes to £1,900.

Now for the mortgage interest. Instead of an expense, she gets a tax credit. This is calculated at 20% of her mortgage interest: £4,000 x 20% = £800.

So, her final tax bill for the property is: £1,900 (Tax) – £800 (Credit) = £1,100. For a deeper dive on how this works, check out our guide on the https://stewartaccounting.co.uk/mortgage-interest-deduction-rental-property/.

Example 2: The Higher Rate Taxpayer

Now, let's look at David. He has the exact same property figures as Sarah, but his main job puts him in the higher rate tax bracket.

His taxable profit is also £9,500. But here's the crucial difference: because this profit falls into his higher rate band, he’s taxed at 40%.

- Tax on Profit: £9,500 x 40% = £3,800

The mortgage interest tax credit is always calculated at the basic rate (20%), no matter what tax band the landlord is in. So, David’s credit is still £800.

His final tax bill is a different story: £3,800 (Tax) – £800 (Credit) = £3,000. This really shows how much your personal tax situation can impact your final bill.

A Quick Comparison

To put this into perspective, let's compare how the tax liability changes based on the landlord's personal tax band, using the same £9,500 rental profit from our examples.

| Example Rental Tax Calculations | |||

|---|---|---|---|

| Taxpayer Type | Taxable Profit | Tax Rate Applied | Total Tax Owed |

| Basic Rate (Sarah) | £9,500 | 20% | £1,100 |

| Higher Rate (David) | £9,500 | 40% | £3,000 |

As you can see, the same rental property can result in vastly different tax bills. It’s a perfect illustration of why personalised advice is so important.

Example 3: Using the Property Allowance

Finally, there’s Maria. She just rents out her garage for storage, bringing in £1,500 a year. Her actual running costs are tiny, only about £150.

Maria has two options:

- Deduct her actual expenses: £1,500 – £150 = £1,350 taxable profit.

- Use the flat-rate £1,000 property allowance: £1,500 – £1,000 = £500 taxable profit.

By choosing the property allowance, Maria slashes her taxable profit from £1,350 to just £500. This saves her money and a lot of record-keeping hassle. It's a fantastic tool for landlords with lower rental incomes and minimal expenses.

Getting to Grips with Your Self Assessment Tax Return

So, you’ve worked out your rental profit. The next job is to report it to HMRC, and that means getting familiar with the Self Assessment system. It can look a bit intimidating at first glance, but once you understand the steps involved, it's a straightforward process.

The secret to a stress-free tax season is knowing what you need to do and when. Missing a deadline lands you with an automatic penalty, so getting those key dates in your diary is an absolute must.

First Things First: Registering for Self Assessment

Before you can even think about filing, you have to tell HMRC you've become a landlord. You are required to register for Self Assessment by 5th October following the end of the tax year you first received rental income.

Let’s say you started renting out your property in July 2024. That falls within the 2024/25 tax year, so your deadline to register would be 5th October 2025. Don't miss this date – it's an easy way to get an unnecessary fine. Once you're registered, HMRC will send you a Unique Taxpayer Reference (UTR) number, which is your key to filing and communicating with them.

The Golden Rule: Meticulous Record-Keeping

A smooth tax return is built on good records. Throughout the year, you absolutely must keep an organised account of every penny coming in and going out. This isn't just to make filling out the forms easier; it's your proof if HMRC ever decides to take a closer look at your figures.

Think of it as building your evidence file. It should contain:

- Proof of Income: Copies of tenancy agreements and bank statements showing rent payments are perfect for this.

- Records of Expenses: Keep every single receipt and invoice for the costs you want to claim against. This covers everything from letting agent fees and insurance to that emergency plumber you had to call out.

- Mileage Logs: Do you use your own car to visit the property or meet tenants? Keep a simple log of your journeys. You can claim a fixed amount per mile, and it all adds up.

Filling Out the SA105 Property Section

When you sit down to do your Self Assessment online, you’ll need to complete the supplementary pages for property income, known as form SA105. This is where you'll lay out all your income and expenses for the taxman.

The SA105 form is where your careful record-keeping pays off. You'll input your total rental income, then break down your allowable expenses into different categories. It’s vital to be accurate here, as these numbers are used to calculate your final taxable profit.

Once you’ve entered all the figures, the form calculates your net profit (or loss). This number is then transferred to your main tax return (the SA100) and added to any other income you might have, like a salary, to work out your total tax bill. For a more detailed walkthrough, our guide to the property rental tax return breaks it down step-by-step.

Paying Your Tax Bill

After filing your return, HMRC will confirm how much tax you owe. The main payment deadline that everyone knows is midnight on 31st January.

However, there's a slight catch for many landlords called Payments on Account. These are essentially advance payments towards your next year's tax bill. If your last Self Assessment bill was over £1,000, you’ll almost certainly have to make them.

The payments are split into two instalments, with deadlines on:

- 31st January: Your first payment for the upcoming tax year.

- 31st July: Your second payment.

This system is designed to help you spread the cost, but it can catch new landlords by surprise. Make sure you budget for these payments so you aren't left scrambling for the funds when the deadlines arrive.

When Should You Call in an Accountant?

It’s tempting to handle your rental accounts yourself, especially when you're just starting out. And for a while, that might work just fine. But as your property business grows, so does the complexity. Sooner or later, you'll reach a tipping point where going it alone becomes more of a liability than a cost-saving measure.

Think of it like this: anyone can put up a shelf, but you’d call a builder to knock down a wall. Property tax works the same way. Managing one straightforward rental is one thing, but juggling a portfolio, selling a property, or navigating new legislation is a whole different ball game. That's when getting an expert on your side isn't just a good idea—it's essential for protecting your investment.

Telltale Signs You Need an Expert

If any of the following scenarios sound familiar, it's a strong signal that it’s time to seek professional advice. It’s far better to be proactive and get things right from the start than to try and fix a costly mistake down the line.

Here are a few common triggers that tell our clients it's time to make the call:

- Your portfolio is growing. Managing one property is manageable. Managing two, three, or more? The paperwork and potential for error multiply fast. An accountant will keep everything organised and make sure your portfolio is structured in the most tax-efficient way possible.

- You're selling a rental property. When you sell, you’ll almost certainly have to deal with Capital Gains Tax (CGT). This is a minefield for the unprepared, with its own specific rules, reliefs, and reporting deadlines. A good accountant can accurately calculate what you owe and legally minimise the final bill.

- You're thinking about using a limited company. Shifting your properties into a limited company can have significant tax benefits, but it’s not the right move for everyone. This is a major structural decision that needs a proper analysis of your personal circumstances and long-term goals—something a property tax specialist is perfectly placed to help with.

- You just don't have the time. Let's be honest, tax is a full-time job. If you’d rather spend your time finding great tenants or scouting your next investment, offloading the tax admin to a professional frees you up to do just that.

How Stewart Accounting Services Can Help

At Stewart Accounting Services, we live and breathe property tax. We work with landlords across the UK every single day, so we’ve seen it all. Our job is to make sure you do pay tax on rental income that you owe, but not a penny more than you absolutely have to.

Our goal is simple: to give you complete peace of mind. We handle the numbers and the compliance so you can get back to what you do best—managing and growing your property business.

Whether it’s getting your Self Assessment sorted using modern tools like Xero or providing strategic advice as you plan your next move, our team is here to translate confusing tax jargon into clear, practical guidance.

If you feel like your property finances are getting a bit too complicated, or you're looking to the future, don't leave it to guesswork. Schedule a consultation with Stewart Accounting Services today and see how we can save you time, stress, and money.

Frequently Asked Questions About Rental Income Tax

Once you've got the basics down, you'll inevitably start thinking about the "what ifs". These are the common scenarios that can trip landlords up, but the rules are usually quite simple once you know them.

Let's dive into some of the most frequent questions we get asked, giving you clear answers to handle these tricky, yet common, situations.

What Happens If My Property Makes a Loss?

It's not uncommon, especially when you're just starting out, for your allowable expenses to outweigh your rental income. When this happens, you have a rental loss. The good news is that this isn't just a sunk cost.

You can carry that loss forward and set it against future profits from the same rental business. Say you make a £2,000 loss this year but turn a £5,000 profit next year. You can use that earlier loss to shrink your taxable profit down to just £3,000. The key is that you must report the loss on your Self Assessment tax return to be able to use it later on.

A crucial point: Always report your losses to HMRC. If you don't, you lose the right to offset them against future profits, which means you could end up paying more tax than you need to down the line.

How Is Tax Handled for Jointly Owned Properties?

When you own a rental property with someone else, whether it's a spouse or a business partner, the profits are usually divided according to your ownership share. For married couples and civil partners, HMRC's default position is a straight 50/50 split, no matter who actually paid for the deposit or mortgage.

However, if you own the property in unequal shares (say, 70/30), you can ask HMRC to tax you on that basis by completing a Form 17. This can be a smart move for tax planning, particularly if one partner pays tax at a lower rate than the other.

Are Furnished Holiday Lettings Different?

Yes, absolutely. Furnished Holiday Lettings (FHLs) play by a completely different set of tax rules, which can be much more generous. To qualify as an FHL, your property has to meet some strict criteria around how often it's available to let and actually occupied.

If it meets the conditions, you unlock tax advantages that aren't available for standard buy-to-lets, including:

- Capital Gains Tax reliefs: You could benefit from reliefs like Business Asset Disposal Relief when you come to sell, significantly lowering your tax bill.

- Capital allowances: You can claim tax relief on the cost of furniture, fixtures, and equipment within the property.

- Pension contributions: The profits you make count as 'relevant earnings', meaning you can make bigger contributions to your pension.

The tax rules for FHLs are a specialist area, so it's a very good idea to get professional advice if you're running one.

Figuring out the finer points of rental income tax can feel like a maze, especially when your circumstances don't fit the standard mould. At Stewart Accounting Services, our team lives and breathes property tax for landlords across the UK. We make sure you're not only compliant but also as tax-efficient as you can be.

Take the guesswork out of your tax return by contacting us today.