The tax on dividends UK business owners face is all about which income tax band they land in. After you've used up your annual Personal Allowance and the specific Dividend Allowance, any dividend income you take will be taxed at 8.75%, 33.75%, or 39.35% for the 2024/25 tax year.

Unpacking the Fundamentals of Dividend Tax

For most directors running their own limited company, getting to grips with dividend tax isn't just a box-ticking exercise—it's the bedrock of smart financial planning. So, what is a dividend? It’s simply a way for a company to share its profits with its shareholders.

Crucially, dividends are paid out after the company has already paid its Corporation Tax bill. This makes them a completely different beast from a salary, which is treated as an allowable business expense. That means a salary is deducted from profit before Corporation Tax is calculated. This distinction is the linchpin for most tax-efficient pay strategies for company owners.

Dividends vs Salary: The Key Tax Differences

Why do so many business owners prefer dividends over a larger salary? It boils down to a couple of major tax advantages.

- No National Insurance: The big one. Neither you nor your company pays a penny of National Insurance Contributions (NICs) on dividends. That’s an instant and significant saving right there.

- Lower Tax Rates: The tax rates you pay on dividend income are considerably lower than the income tax rates charged on salary.

When you put those two benefits together, a low-salary, high-dividend strategy often becomes the most sensible way to pay yourself. If you're keen to explore this further, our guide explains in detail how dividends work and how much you can take.

The Core Concepts You Need to Know

To get your head around the tax on dividends in the UK, there are two concepts you absolutely have to understand: the Dividend Allowance and the tax bands.

Think of the Dividend Allowance as a specific tax-free bubble for your dividend income each year. It’s an amount you can receive without paying any tax on it.

But it’s not quite as simple as a straightforward deduction. This allowance still uses up a portion of your income tax band. Getting a feel for metrics like how to calculate dividend yield can also help build a fuller picture of how your shares are performing.

It’s all about the 'stacking' principle. HMRC looks at your total income—from salary, self-employment, property, and finally, dividends—and stacks it all together. Where your dividend income lands in that stack determines which tax rate applies.

Understanding how these pieces fit together is the key. In this guide, we'll walk you through exactly how it all works, giving you the knowledge you need to manage your money with confidence.

How the Dividend Allowance Really Works

Lots of people get the Dividend Allowance wrong. It’s easy to think of it as a simple deduction, like money off your tax bill, but the reality is a bit more subtle.

The best way to think about it is as a special 0% tax band. It’s a dedicated, tax-free zone for the first chunk of your dividends each year. Any dividend income that falls within this allowance is taxed at zero. Simple enough, right?

But here’s the crucial detail that catches so many people out: even though you don’t pay tax on it, that income still uses up a slice of your income tax band. This is the key. While the allowance saves you tax on that first bit of dividend income, it can push your other income—or any dividends you receive above the allowance—into a higher tax bracket much sooner.

The Ever-Shrinking Allowance

This tax-free zone for dividends hasn't always been so small. In fact, its rapid reduction is why tax planning has become so vital for company directors and investors. The history here tells a clear story.

Before the 2016/17 tax year, the old tax credit system meant basic rate taxpayers didn't really pay any extra tax on their dividends at all. That world is long gone. It was replaced by a £5,000 Dividend Allowance, which has been chipped away ever since. It was slashed to £2,000 in 2018, halved to £1,000 in 2023, and now sits at a mere £500 from the 2024/25 tax year onwards.

That’s a 90% drop from where it started. It’s a huge squeeze, particularly for small business owners who rely on a dividend-based income. For a deeper dive into this shift, the LITRG website offers some great analysis.

What this means in real terms is that far more of your dividend income is now subject to tax. If you're a director taking £30,000 in dividends, the allowance cuts alone mean you're now paying tax on an extra £4,500 compared to a few years ago.

Stacking Up Your Income: How It All Fits Together

So, how does this work in practice? It all comes down to the order in which HMRC looks at your income. They follow a strict "stacking" principle:

- First, they look at your non-savings, non-dividend income. This is usually your salary, self-employed profits, or rental income.

- Next up is any savings income, like interest from a bank account.

- Finally, right at the top, comes your dividend income.

Your Personal Allowance (£12,570 for 2024/25) gets used up first, almost always against your salary. Only after that’s gone does the Dividend Allowance kick in against your dividend income.

Let's try an analogy. Picture your tax bands as big buckets (basic, higher, and additional rate). You start filling the basic rate bucket with your salary.

Think of your Dividend Allowance as a small, tax-proof box. You have to place this box inside the bucket, right on top of your salary. The dividends inside that box are protected from tax, but the box itself still takes up physical space, pushing you closer to the brim.

For instance, say your salary fills up the first £20,000 of your basic rate band. Your £500 Dividend Allowance then sits on top of that, occupying the slice from £20,001 to £20,500. It’s tax-free, but it’s used up that part of the band. Any further dividends you receive will start being taxed from £20,501 onwards. It’s a subtle point, but understanding it is fundamental to getting your UK dividend tax calculation right.

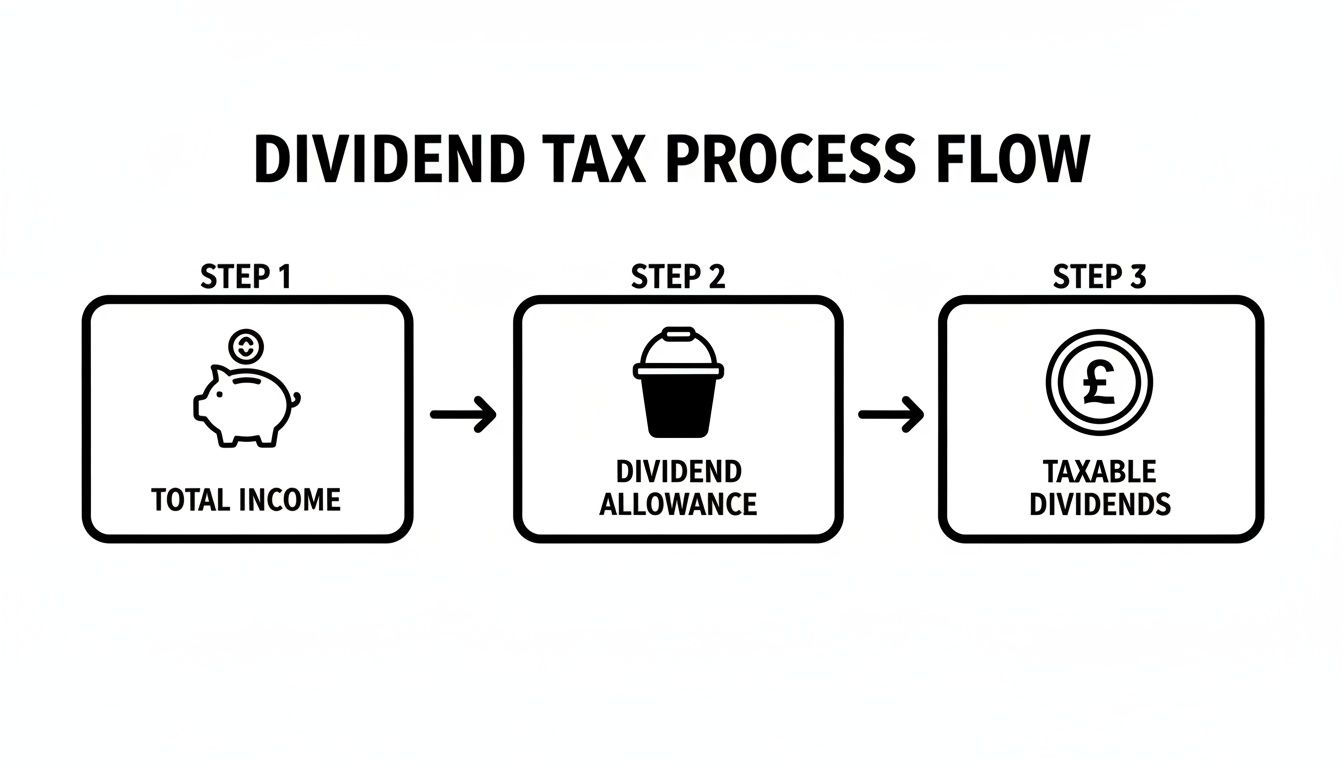

A Practical Guide to Calculating Your Dividend Tax

Figuring out your dividend tax bill can feel like a bit of a headache at first, but it's a lot simpler once you break it down. Don't try to tackle it as one giant calculation. Instead, think of it as a series of small, manageable steps that build on each other.

The basic idea is to work out your total income for the year, deduct your tax-free allowances in the correct order, and then see which tax bands your dividends fall into. Follow this process, and you'll get an accurate picture of what you owe under the UK's dividend tax rules.

The Five Steps to Your Calculation

To get to the final number, you need to follow a specific sequence. HMRC doesn't look at your dividend income on its own; it gets stacked right on top of everything else you earn.

Here’s the five-step process that I always follow:

-

Work Out Your Total Income: First things first, add up every penny you've earned in the tax year. This means your salary, any self-employed profits, rental income, and, of course, the total dividends you've received before any tax.

-

Deduct Your Personal Allowance: Next, subtract your Personal Allowance (currently £12,570) from your total income. This is almost always applied to your non-dividend income first, like your salary.

-

Stack Your Income Against Tax Bands: This is the most important—and often misunderstood—part. You have to layer your income types into the tax bands in a strict order: non-savings income (like your salary) goes first, then any savings income, and finally, your dividend income sits at the very top.

-

Apply the Dividend Allowance: Once you know where your dividend income begins, you can apply your tax-free Dividend Allowance, which is currently £500. This chunk is taxed at 0%, but it's crucial to remember that it still uses up a portion of the tax band it falls into.

-

Apply the Correct Tax Rates: Any dividend income you have left over—above the allowance—is then taxed at the rate for whichever band it sits in. This will be the basic, higher, or additional rate.

This flowchart gives you a great visual of how everything flows, from your total income down to the final taxable amount.

As you can see, your total income is just the starting point. The allowances are peeled away one by one before any tax rates come into play.

Understanding the Income Stacking Rule

That "stacking" rule in step three? It's everything. Getting this wrong is the single most common mistake I see people make when calculating their dividend tax. You can't just look at your dividends in a vacuum; where they sit in your overall income stack determines the rate you pay.

Think of your tax bands like containers of different sizes. You have to fill them in a set order. Your salary goes in first, filling the basic rate container from the bottom up. Your dividend income is then poured in on top, filling whatever space is left and potentially spilling over into the next, higher-taxed container.

This is exactly why the classic small salary, big dividend structure can be so tax-efficient. The salary uses up the Personal Allowance and a small slice of the basic rate band, leaving as much of that lower-taxed space as possible free for your dividends.

Why Every Pound Matters Now

In recent years, the goalposts have moved quite a bit. With the Dividend Allowance slashed to just £500, even fairly modest dividend payments can now attract tax if your total income pushes you past the Personal Allowance. The changes have really squeezed limited company directors who rely on dividends for their income.

It's no longer a case of 'set and forget'. Proactive planning is now essential to make sure you're not accidentally tipping yourself into a higher tax band. To see just how much things have changed, it's worth taking a look at the government's historical income tax data.

Real-World Dividend Tax Calculation Examples

The theory is one thing, but the best way to really get your head around the tax on dividends UK rules is to see them play out in practice. Let's crunch the numbers for three common scenarios in the 2024/25 tax year to see how it all comes together.

These examples are great because they show how different types of income—like a salary or rental profits—interact with your dividend income. You'll see exactly how the "income stacking" principle works and why the order in which you account for your earnings matters so much.

Example 1: The Limited Company Director

First up, meet Sarah. She's the director of a successful consultancy and uses the classic low-salary, high-dividend strategy to keep her tax bill efficient.

Here's her income for the year:

- Salary: £12,570 (set to perfectly match her Personal Allowance)

- Dividends: £50,000

Let's work out her total tax liability.

Her total income for the tax year is simply £62,570 (£12,570 salary + £50,000 dividends).

Because her £12,570 salary is completely covered by her Personal Allowance, she pays no income tax on it. However, this uses up her entire Personal Allowance, meaning all her dividends are potentially taxable.

Now for the dividends. We stack these on top of her salary:

- The first £500 of her dividends is covered by the tax-free Dividend Allowance. No tax is due here.

- The next chunk of dividends falls into the basic rate band, which ends at £50,270. She has already used up the first £12,570 of this with her salary, and the first £500 with the dividend allowance. So, the amount of dividends taxed at the basic rate is £37,200 (£50,270 – £12,570 – £500).

- This portion is taxed at the basic dividend rate of 8.75%.

- The rest of her dividends (£50,000 – £500 – £37,200 = £12,300) are pushed into the higher rate tax band.

- This final amount is taxed at the higher dividend rate of 33.75%.

Sarah’s Total Dividend Tax Bill:

(£37,200 x 8.75%) + (£12,300 x 33.75%) = £3,255 + £4,151.25 = £7,406.25

As you can see, even though her salary is tax-free, it still plays a crucial role by pushing a significant portion of her dividend income into the higher tax bracket.

Example 2: The Contractor with Fluctuating Income

Next, we have David, an IT contractor working through his own limited company. His income can be a bit up and down depending on the projects he lands. This year, he’s taken a smaller salary and more modest dividends.

Here's his setup:

- Salary: £9,100 (this is high enough to earn National Insurance credits but low enough to avoid paying any contributions)

- Dividends: £35,000

David's total income is £44,100 (£9,100 + £35,000).

His £12,570 Personal Allowance easily covers his entire £9,100 salary. Better yet, he has £3,470 of his Personal Allowance left over (£12,570 – £9,100). He can use this remainder against his dividend income, making the first £3,470 of his dividends completely tax-free as well.

Let's calculate the tax on the rest of his dividends:

- The first £500 of his remaining dividends are covered by his tax-free Dividend Allowance.

- This leaves £31,030 of dividends to be taxed (£35,000 – £3,470 – £500).

- Since his total income of £44,100 is well under the higher rate threshold of £50,270, this entire amount falls within the basic rate band.

- The tax is calculated at 8.75%.

David’s Total Dividend Tax Bill:

£31,030 x 8.75% = £2,715.13

By keeping his total income below the higher rate threshold, David avoids the much steeper 33.75% tax rate entirely.

Example 3: The Landlord with a Side Portfolio

Finally, let's look at Maria. She's a landlord who earns most of her income from property, but she also has a small portfolio of UK shares that pay her dividends.

Her income breakdown is:

- Rental Profit: £40,000

- Dividends: £6,000

Maria's total income is £46,000 (£40,000 + £6,000).

The tax system prioritises non-savings income, so her £12,570 Personal Allowance is first set against her rental profit. This leaves her with a taxable rental profit of £27,430 (£40,000 – £12,570), which will be taxed at the standard income tax rates.

Her £6,000 in dividend income is then stacked on top of her £40,000 rental income.

- The first £500 of these dividends is covered by the Dividend Allowance, so it's taxed at 0%.

- The remaining £5,500 of dividends (£6,000 – £500) still falls within the basic rate band, because her total income of £46,000 is below the £50,270 higher rate threshold.

- This remaining amount is therefore taxed at the basic dividend rate of 8.75%.

Maria’s Total Dividend Tax Bill:

£5,500 x 8.75% = £481.25

This scenario is a perfect illustration of how your main income source effectively sets the stage, determining which tax band your dividends will ultimately fall into.

How to Report and Pay Dividend Tax to HMRC

Working out what dividend tax you owe is a big step, but it's really only half the job. Next, you need to report this income to HMRC and settle the bill. For most company directors and investors, this all happens through the Self Assessment tax return system.

It’s one of those bits of admin you simply can’t afford to ignore. Missing deadlines triggers automatic penalties, interest charges, and a whole load of stress you just don't need. The secret is to know your obligations and key dates inside out, so you can stay compliant and focus on what you actually enjoy—running your business.

Using the Self Assessment System

If you have dividend tax to pay, you will almost certainly need to file a Self Assessment tax return. This is HMRC’s standard system for declaring any income that hasn't already been taxed at source, which is the case for dividends (unlike a PAYE salary).

The whole process boils down to a few key steps, each with a firm deadline.

- Register for Self Assessment: If you’ve never filed a return before, you must register by 5th October after the end of the tax year you received the dividends in.

- File Your Tax Return: The cut-off for getting your online tax return submitted is midnight on 31st January the following year.

- Pay Your Tax Bill: Your payment deadline is the same day—31st January.

Miss any of these dates and you're looking at instant penalties, so it's a good idea to get them in your calendar right away. For a full walkthrough of the forms and what’s involved, take a look at our detailed guide to completing a Self Assessment tax return.

Deadlines and the Danger of Delay

I can't stress enough how important it is to be proactive. A classic example of this was back in 2016 when the dividend tax rules changed. Thousands of company directors rushed to pay themselves large dividends to get ahead of the new, higher tax rates. The Office for Budget Responsibility calculated that this last-minute dash added £4.0 billion to the tax haul, which just goes to show how many people scrambled to avoid the hike. It's a perfect lesson in why acting early beats reacting late every time. You can read more on the impact of this income shifting on OBR.uk.

The stakes are just as high today. With allowances shrinking, leaving things to the last minute can easily cost you thousands. Being organised and planning your dividends well in advance is the best way to make sure you're not paying more tax than you have to.

How to Make Your Payment

Once you’ve filed your return and have your final tax figure, HMRC gives you a few different ways to pay. Just pick the one that suits you best.

Common Payment Options:

- Online bank transfer (via Faster Payments)

- Debit card on the HMRC online portal

- At your bank or building society, using a paying-in slip from HMRC

- Direct Debit, though you'll need to set this up well in advance

Whatever method you choose, make sure you leave enough time for the payment to clear, which can take a few working days. Trying to pay on the afternoon of the 31st of January is just asking for trouble! For many business owners, this is exactly the sort of compliance headache that makes getting an accountant on board a complete no-brainer.

Smart Tax Planning for Company Directors

Once you've got a handle on the rules, you can start thinking about how to legally and ethically reduce the amount of tax you pay on your dividends. This isn't about finding secret loopholes; it's about using the tax system intelligently to keep more of your hard-earned profit.

For most directors of limited companies, this boils down to being strategic about how you take money out of the business.

The Go-To Strategy: Low Salary, High Dividends

By far the most common approach is the low-salary, high-dividend model. The logic behind it is refreshingly straightforward: you pay yourself a small salary, just enough to stay "on the books" for state benefits, and then draw the majority of your income as dividends.

This works so well for two main reasons:

- No National Insurance: Dividends are not subject to National Insurance Contributions (NICs) at all. A salary, however, gets hit with both employee's and employer's NICs once you go over the threshold. That's a huge saving right there.

- Lower Tax Rates: Dividend tax rates (8.75%, 33.75%, and 39.35%) are significantly lower than their income tax equivalents (20%, 40%, and 45%).

By keeping your salary at an optimal level—often around the National Insurance threshold—you can build up qualifying years for things like the State Pension without actually paying any NICs. You then take the rest of your income via dividends, benefiting from those lower tax rates. Our in-depth guide offers a detailed look at the pros and cons of salary versus dividends.

Other Tools for Your Tax-Planning Kit

While the low-salary, high-dividend method is the foundation of smart tax planning for many directors, it’s not the only option. Think of it as the main tool, but you can get even better results by combining it with others.

Think of your tax planning like assembling a toolkit. The low-salary, high-dividend model is your trusty hammer, but sometimes you need a screwdriver or a wrench to get the job done perfectly. Building a complete set of tools gives you the flexibility to adapt to any financial situation.

Here are a few other powerful methods worth considering:

- Use Your Spouse's Allowances: If your spouse or civil partner is a basic rate taxpayer or has unused allowances, making them a shareholder could be a great move. You can then pay them dividends, making use of their tax-free allowances and keeping more of the family's total income out of the higher tax bands.

- Make Pension Contributions: Paying into your pension directly from the company is one of the most tax-efficient things you can do. The contribution reduces your company's profit, lowering its Corporation Tax bill, and the money grows in your pension pot tax-free.

- Take Advantage of ISAs: You can hold dividend-paying shares inside a Stocks and Shares ISA. Any dividends you earn from these investments are completely sheltered from dividend tax. It's a fantastic way to grow your investments without worrying about the taxman.

Beyond these specific tax tactics, exploring broader powerful dividend investing strategies can also help maximise your overall returns.

Ultimately, there's no single "best" approach—it all comes down to your individual circumstances. While these are common and effective strategies, getting professional advice is the best way to build a plan that's perfectly aligned with your financial goals.

Common Questions About UK Dividend Tax

Working with dividends often brings up the same handful of questions, even when you think you've got the basics down. Some of the rules have nuances that can catch people out. Let's run through some of the most common queries to clear up any lingering confusion.

Think of this as your quick-fire FAQ round to make sure you’re completely clear on how things work in practice.

Do I Pay National Insurance on Dividends?

Here’s some good news: absolutely not. Dividends are completely free from National Insurance Contributions (NICs), for both the employee and the employer.

This is probably the single biggest reason why taking dividends is so popular compared to a salary. For the 2024/25 tax year, an employee faces an 8% NICs hit on most of their salary, and the company gets stung with a 13.8% employer's contribution on top. With dividends, all of that disappears. It's the cornerstone of tax-efficient profit extraction for a reason.

How Does Scottish Income Tax Affect My Dividend Tax?

This one trips a lot of people up, but the answer is surprisingly simple: it doesn't.

Dividend tax is handled on a UK-wide basis. That means the income tax bands used to work out your dividend tax rates are the same whether you live in England, Scotland, Wales, or Northern Ireland.

A Scottish taxpayer will pay different income tax rates on their salary, but when it comes to dividends, their income is measured against the standard UK-wide bands. Your postcode doesn’t change the rate of tax on your dividends.

So, it doesn't matter if you're in Aberdeen or Bristol. The threshold for higher-rate dividend tax still kicks in at £50,270, and the additional rate starts at £125,140 for everyone.

Can I Declare a Dividend Whenever I Want?

Not quite. While dividends offer fantastic flexibility, you can't just decide to pay yourself on a whim. There’s a critical legal hurdle you have to clear first.

A limited company is only allowed to pay a dividend if it has enough retained profits to cover it. These are the profits left in the business after you’ve paid your Corporation Tax bill. Think of it as the company’s accumulated savings from this year and previous years.

If you declare a dividend without enough retained profit in the bank, it’s considered an 'illegal' or 'ultra vires' dividend. HMRC takes this very seriously, and it can create a real mess, potentially leaving the director personally liable. This is exactly why keeping your books accurate and up-to-date isn't just good admin—it's a legal must-have for any director.

At Stewart Accounting Services, we help business owners across Central Scotland and the UK get to grips with Corporation Tax and smart dividend planning. Our goal is to make sure you can take profits out of your business efficiently and stay on the right side of the rules, giving you more time, more money, and a clearer mind. See how our expert team can help your business thrive at https://stewartaccounting.co.uk.